Over the years and previous decades, mortgage interest rates have changed in accordance with the Bank of England base rate.

Below we explore the trends and factors that impacted them and how things may look in the future.

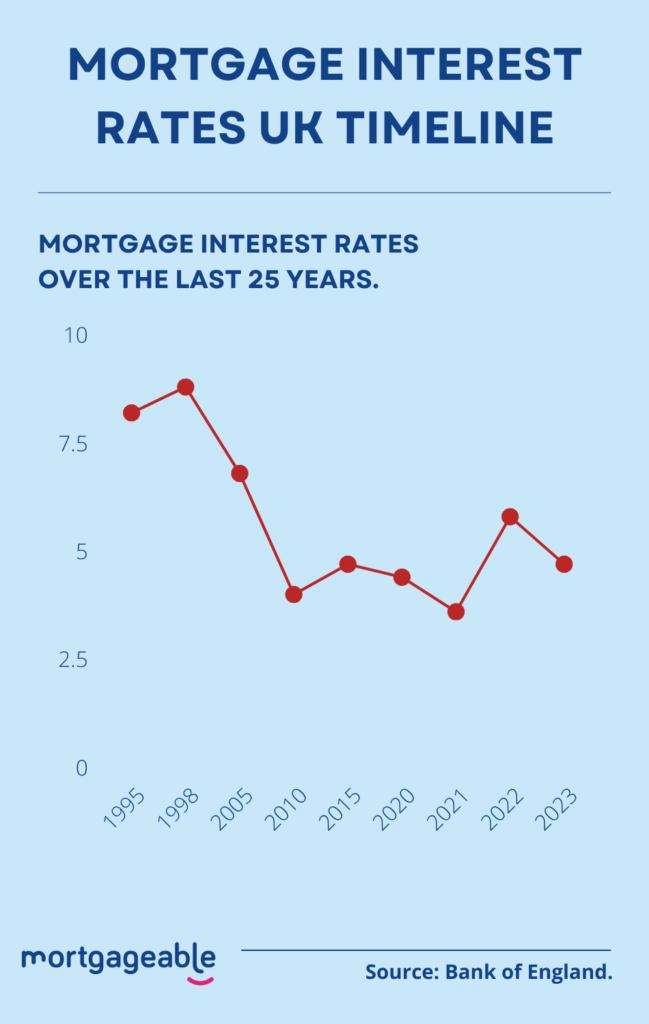

The infographic below shows the mortgage rate history in the UK over the last 25 years and includes the highest and lowest average annual interest rates recorded during that timeframe.

From 1995 until 2022, the average mortgage interest rate in the UK averaged 5.62%.

In the last 25 years, the average mortgage interest rate peaked at 8.87 percent in September of 1998.

In the last 25 years, the average mortgage interest rate was at its lowest in September 2021, at which point it was 3.59 percent.

It’s important to be aware that in the short term changes in mortgage interest rates don’t impact current mortgage borrowers, since the majority are on a fixed term mortgage.

In fact, around 75% of mortgage borrowers are on a fixed term mortgage and in 2019 over 90% of new mortgage borrowers opted for a fixed term mortgage.

A fixed-rate mortgage is a mortgage with a specific interest rate locked in for a certain duration e.g. 2, 4 or 10 years.

Therefore, the majority of people i.e. those on a fixed rate mortgage will see no change in their mortgage payments in the short term.

Those who are most vulnerable to changes to the interest rates are the over 850,000 individuals on a variable rate mortgage.

In practical terms, UK Finance estimates that a rise in the Bank Rate of 0.15 percentage points will lead to an average increase in repayments by £15.45 per month.

Although your actual mortgage rate will be determined by factors like the product you choose and your particular lender, the Bank of England’s base rate also has a major impact to mortgage interest rates.

The base rate doesn’t just impact mortgages, but a wide range of financial products, as well as the value of the pound itself.

The Bank of England review the base rate on the first Thursday of every month and may be changed depending on the rate of spending in the economy.

For example, if spending is deemed to be too low, the base rate will be decreased and if it’s too high, it will be reduced.

| Bank rate at year end (%)* | |

| 1979 | 17 |

| 1980 | 14 |

| 1981 | 14.375 |

| 1982 | 10 |

| 1983 | 9.0625 |

| 1984 | 9.5 |

| 1985 | 11.375 |

| 1986 | 10.875 |

| 1987 | 8.375 |

| 1988 | 12.875 |

| 1989 | 14.875 |

| 1990 | 13.875 |

| 1991 | 10.375 |

| 1992 | 6.875 |

| 1993 | 5.375 |

| 1994 | 6.125 |

| 1995 | 6.375 |

| 1996 | 5.9375 |

| 1997 | 7.25 |

| 1998 | 6.25 |

| 1999 | 5.5 |

| 2000 | 6 |

| 2001 | 4 |

| 2002 | 4 |

| 2003 | 3.75 |

| 2004 | 4.75 |

| 2005 | 4.5 |

| 2006 | 5 |

| 2007 | 5.5 |

| 2008 | 2 |

| 2009 | 0.5 |

| 2010 | 0.5 |

| 2011 | 0.5 |

| 2012 | 0.5 |

| 2013 | 0.5 |

| 2014 | 0.5 |

| 2015 | 0.5 |

| 2016 | 0.25 |

| 2017 | 0.5 |

| 2018 | 0.75 |

| 2020 | 0.25 |

| 2020 | 0.10 |

| 2021 | 0.25 |

| 2022 | 0.5 |

| 2022 | 0.75 |

| July 2023 | 5.0 |

Source: Bank of England Official Bank Rate History

As of December 2022, the Bank of England base rate stands at 3.5%.

According to Trading Economics latest data the average mortgage rate was 5.88% as of December 2022.

However, as mentioned this is an average and the exact rate offered to you will depend on a range of factors including your credit score, the mortgage lender, type of mortgage etc.

According to Trussle, at present, the average cost of two- and five-year fixed rate deals across all deposit levels stands at 5.37% and 4.84% respectively.

The Bank of England increase the base rate in order to “cool” the economy and control surging inflation.

In October, the Consumer Prices Index (CPI) measure of inflation rose to a heady 11.1% in the 12 months to October, in direct conflict with government targets of 2% inflation.

Unfortunately, if inflation does not start to fall, the Bank of England could decide to continue to increase rates into the new year.

The cost of energy is another major contributor to surging inflation, but thanks to the UK government’s Energy Price Guarantee this has been tempered to a large degree.

Recommended guides:

With interest rates changing regularly, there is a lot of volatility in the market at present with mortgage deals being constantly updated to reflect the rapid pace of change.

With this in mind, it’s now unarguably more true than ever that you should contact a mortgage broker for help and advice.

A mortgage broker or advisor can hold your hand through the entire process, from initial searches to dealing with the legal stuff, to ensure the process is as smooth as possible.

Call us today on 03330 90 60 30 or contact us. One of our advisors can talk through all of your options with you.

AS A MORTGAGE IS SECURED AGAINST YOUR HOME, IT COULD BE REPOSSESSED IF YOU DO NOT KEEP UP THE MORTGAGE REPAYMENTS.

Mortgageable is a trading style of Respective Financial Services Limited who are authorised and regulated by the Financial Conduct Authority 998434 registered in England and Wales No: 14687578. Registered Office: The Old Rectory, Winwick, WA2 8LE. Calls may be recorded for training and monitoring.

Mortgageable does not arrange or advise on Second Charge Mortgages.

A summary of our internal complaints handling procedures for the reasonable and prompt handling of complaints is available on request and if you cannot settle your complaint with us, you may be entitled to refer it to the Financial Ombudsman Service at www.financial-ombudsman.org.uk or by contacting them on 0800 023 4567.

Copyright © Mortgageable 2024. All rights reserved. Privacy Policy.